It Just Got Even Harder to Trust Financial Advisers – (as published on Bloomberg.com)

March 1, 2016 — 12:47 PM EST

There’s a phrase no one wants to read in a sweeping report about the financial advisers who handle their savings: economy-wide misconduct.

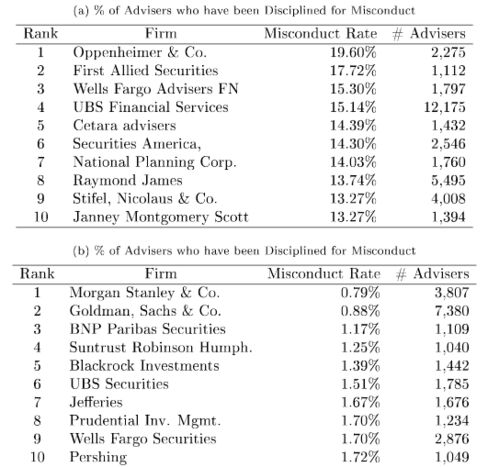

A new working paper by business school professors at the University of Chicago and University of Minnesota found that 7 percent of financial advisers have been disciplined for misconduct that ranges from putting clients in unsuitable investments to trading on client accounts without permission. That’s a troubling mark for an industry that relies on the trust of clients. And some large, well-regarded firms have misconduct records that far exceed the average. Nearly 20 percent of financial advisers at Oppenheimer & Co., with more than 2,000 advisers counted in the study, have misconduct records, according to the new paper.

“It’s everywhere, not just small firms. It is pervasive,” said Amit Seru, a finance professor at the University of Chicago’s Booth School of Business and a co-author of “The Market for Financial Adviser Misconduct.”

Seru considers the study to be conservative in measuring misconduct. The paper homed in on just six of 23 categories of disclosure in the BrokerCheck database considered “indicative of adviser misconduct.” The database is overseen by the Financial Industry Regulatory Authority, or FINRA, the industry’s self-regulatory organization. The study counted as misconduct disclosures about an “investment-related arbitration or civil suit … that resulted in an arbitration or civil judgment for the customer,” as well as formal proceedings by regulators “for a violation of investment-related rules,” among other alleged infractions.

A spokeswoman for Oppenheimer, Jacqui Emerson, said in a statement that the company “has made significant investments to proactively tackle risk and compliance issues in our private client division. We’ve made changes in senior leadership, branch managers, and significant changes in our advisor ranks.” Those reforms include the appointment of a new global compliance officer and efforts to improve surveillance.

Misconduct isn’t left unchecked by financial firms. About half of advisers found to have committed misconduct are fired—although 44 percent of advisers who leave a job due to misconduct are hired by another firm within a year, according to the paper. Many fired advisers end up moving to firms that have higher rates of misconduct than their previous employer did, and they become repeat offenders. “Prior offenders are five times as likely to engage in new misconduct as the average financial adviser,” the study found.

“This is eye-opening and suggests not only that some firms have a high tolerance for misconduct on the part of their employees, but that their very business model is to attract the broker who can generate high revenue at the cost of repetitive disciplinary violations,” said John Coffee, a professor at Columbia Law School in New York. “FINRA needs to focus on this.”

The first-of-its-kind study names names, listing 10 advisory firms with the highest misconduct rates, as well as those with the lowest.

Representatives from firms listed among those with the highest rates of misconduct either declined to discuss the report on the record or did not respond to requests.

FINRA spokesman Ray Pellechia noted in an e-mail that while the organization hasn’t had time to review the working paper, addressing the culture of securities firms is one of FINRA’s top priorities. The regulator “keeps close tabs on potentially high-risk registered persons—and the firms that hire them,” Pellechia said. In 2015, he noted, FINRA permanently barred nearly 500 individuals and 25 firms from the industry. Not all disclosures indicate regulatory problems; for example, Pellechia said, an arbitration complaint that has been dismissed is still disclosed in the database.

Many cases of misconduct arose around the issue of the “suitability” of investments. That would mean, for instance, that an adviser should not suggest that a 75-year-old client put most assets in a high-fee, aggressive-growth mutual fund. Often, the report found, investments involved in reported misconduct cases were insurance products.

Previous studies have raised concerns over conflicted retirement planning advice from financial advisers. Last year, for instance, the President’s Council of Economic Advisors sounded the alarm on bad advice without describing it as an issue of misconduct. “Right now,” its report warned, “your financial advisor—someone who’s supposed to be acting in your best interest—can direct you toward a high-cost, low-return investment rather than recommending a quality investment that works better for you.” The report found that conflicts of interest by advisers likely led to $17 billion of losses annually for working-class and middle-class families.

Some observers believe conflict issues would be alleviated under a new rule that requires all advisers to act as “fiduciaries” in giving retirement advice—to act in their clients’ best interests. Justifying the sale of high-commission products, when there are low-fee alternatives, would become difficult. The rule, which came out of the Department of Labor, has been wending its way through the political process.

One reason why advisers with misconduct records stay in business is a lack of consumer sophistication. “Misconduct is concentrated in firms with retail customers and in counties with low education, elderly populations and high incomes,” the report states. The study’s findings “suggest that some firms ‘specialize’ in misconduct and cater to unsophisticated consumers.”

Since all this adviser data is public, Seru says he is surprised it took so long for someone to do this kind of study. His next project will look at whether greater disclosure efforts in the financial-adviser industry, such as BrokerCheck, help spark better governance.

If you have questions concerning your financial adviser’s or stock broker’s disciplinary record or if you believe that you are the victim of financial misconduct, please call Florida Securities Attorney Greg Tendrich at 561.475.1332.